4. Algorithm Comparison in Optimal Consumption Problem#

DING Minjie, Spring 2025

Differnet algorithm leads to different compuation speed. In this tutorial, I will firstly show computation difference with a simple example. Then, I will compare three methods to solve optimal consumption problem.

A simple example to show computation difference

Optimal Consumption Solution 1: Value Function Iteration using Loop

Optimal Consumption with Income Shock

Optimal Consumption Solution 2: Speed Up with Vectorization

Endogenous Grid Method

Optimal Consumption Solution 3: Speed Up with Endogenous Grid Method

1. A simple example to show computation difference#

Some commonly used methods to speed up computation include:

Vectorization is faster than Loop.

Endogenous grid method is faster than value exogenous grid method.

Use parpool to handle large dataset.

I use optimal consumption as an example to demonstrate speed difference.

cd"C:\Users\ading\A_TA_Notes"

pwd

ans = 'C:\Users\ading\A_TA_Notes'

clear all; % Clears all variables from the workspace

close all; % Closes all open figure windows

clc; % Clears the Command Window

We want to sum up all dot product of elements in a matrix.

rng(100); % Set random seed

n = 1200;

A = random('Normal',0,1,n,n); % Generate Matrix

A = A + A'; % Make it symmetric

The first method is to use nested loops

% Code 1: Nested Loops for Total Calculation

tic; % Start the timer

total_1=0;

for i=1:n

for j=1:n

total_1=total_1+A(i,:)*A(j,:)';

end

end

toc; % End the timer

total_1

历时 4.272858 秒。

total_1 = 3.0207e+06

We can also loop over another dimension.

% Code 2: Another Nested Loop Approach

tic;

total_2=0;

for i=1:n

for j=1:n

total_2=total_2+A(:,i)'*A(:,j);

end

end

toc;

total_2

历时 1.985000 秒。

total_2 = 3.0207e+06

However, loop one by one is slow. We can speed up with vectors.

% Code 3: Vectorized Approach

tic;

total_3=sum(sum(A*A'));

toc;

total_3

历时 0.049618 秒。

total_3 = 3.0207e+06

As we can see, vectorized approach takes much less time.

parpool#

parpool enables us to handle several process simultaneously.

However, it needs initialization time. So, when dealing with small dataset, parpool may not be the fastest.

I have 6 par working together, but the time is longer than 1/6 of normal loops.

Use parpool when we encounter large dataset.

%% Paralell Computing

parpool;

tic; % Start the timer

total_1=0;

parfor i=1:n

for j=1:n

total_1=total_1+A(i,:)*A(j,:)';

end

end

toc; % End the timer

正在使用 'Processes' 配置文件启动并行池(parpool)...

已连接到具有 6 个工作进程的并行池。

历时 1.518947 秒。

2. Optimal Consumption Solution 1: Value Function Iteration using Loop#

Optimal consumption is a classical dynamic programming problem in economics.

The problem can be formally described as follows:

Objective: Maximize the expected utility over time:

\[ V(A) = \max_{c} \left\{ U(c) + \beta E[V(A') | A] \right\} \]where:

V(A): Value function representing the maximum utility achievable with current assets \( A \).

U(c): Utility derived from consumption \( c \). For simplicity, assume \(U(c) = log(c)\).

A’: Future assets after consumption is made,

Asset Transition: determined by the equation:

\[ A' = (1 + r)A + Y - c \]where:

r: is the interest rate

Y: is the income.

Constraints:

\[ c \geq 0 \quad \text{and} \quad c \leq A + Y \]

%% Preparation

% Households

y = 1; % Fixed income received by the agent

gamma = 1; % risk aversion in consumption utility function

r = 0.03; % The rate at which savings grow

beta = 0.95; % How much future utility is worth today

% Assets grids

a_grid_size = 500; % Number of asset grid

a_max = 20; % Maximum value of asset

borrow_limit = 0; % Borrowing limit

a_grid_power = 1; % Power of grid interval, 1 for linear, 0 for L-shaped

a_grid = linspace(0,1,a_grid_size)';

a_grid = a_grid.^(1./a_grid_power);

a_grid = borrow_limit + (a_max - borrow_limit).*a_grid;

% Iteration setting

iter_max = 100; % maxium iteration

iter_counter = 1; % iteration counting

iter_tolerance = 0.01; % Tolerance for convergence

iter_diff = 1; % initial difference

%% Local Function to Facilitate Expression

% Utility function

if gamma == 1

u = @(c)log(c);

else

u = @(c)(c.^(1-gamma)-1)./(1-gamma);

end

% Derivative of utility function to consumption

u1 = @(c) c.^(-gamma);

%% Initialize value functions and consumption function

V_guess = u(r.*a_grid+y)./(1-beta); % initial guess of value function

V_current = zeros(a_grid_size,1); % current value functions from iteration

V_next = zeros(a_grid_size,1); % new value functions from iteration

C = zeros(a_grid_size,1); % consumption policy

V_intermediate = zeros(a_grid_size, iter_max); % intermediate value functions

%% Iteration using fmincon

options = optimoptions('fmincon','Display','off','TolX',1.0e-8); % Options for the optimizer

tic

while iter_counter <= iter_max && iter_diff > iter_tolerance

for i = 1:a_grid_size

utility_function = @(c) - u(c) - beta * interp1(a_grid, V_current, (1+r)*(a_grid(i) + y - c));

% we need to find maximum utility, and we have fmincon

% so we try to find minimum negative utility

% interpolated from the current value function.

[C(i), V_next(i)] = fmincon(utility_function, y + 0.5 * a_grid(i),[],[],[],[],eps,a_grid(i) + y, [], options);

% [x,fval] = fmincon(fun,x0,A,b,Aeq,beq,lb,ub,nonlcon,options)

% find c(i) and V'(i) that maximize utility

% x0 = income+0.5*assetGrid(i)

% upper bound = assetGrid(i)+income

end

% Update value function

V_next = -V_next;

V_intermediate(:,iter_counter) = V_next;

iter_diff = max(abs(V_current - V_next));

V_current = V_next;

iter_counter = iter_counter + 1;

end

% Displays the total number of iterations and the time taken

fprintf('Total iteration: %3i, Time: %2.6f \n', iter_counter, toc);

Total iteration: 31, Time: 48.294024

Here are parameters which will affect total running time of iteration.

a_grid_size: number of total grid

a_grid_power: interval difference of grid

gamma: type of utility function, when gamma doesn't equal to 1, the computation is more complicated.

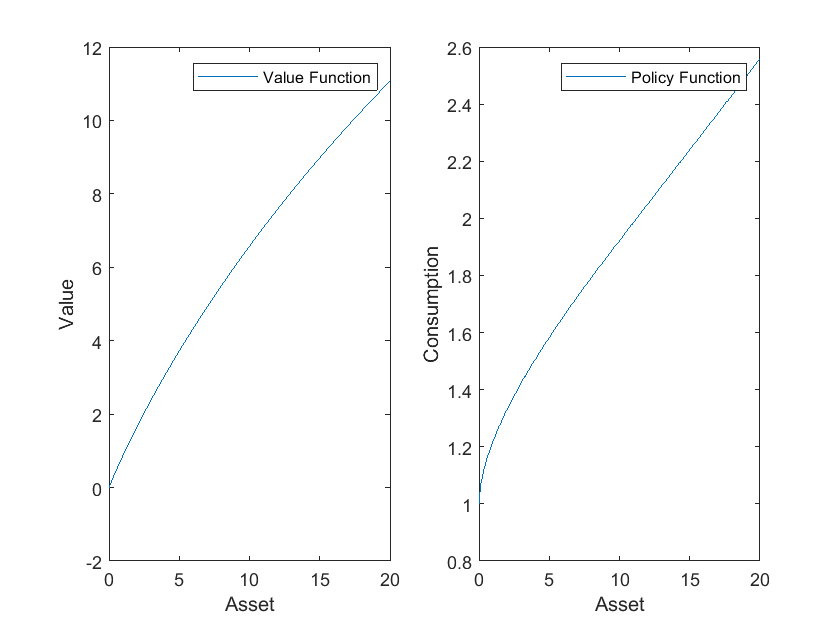

%% Plotting

figure(1)

subplot(1,2,1)

plot(a_grid,V_current)

legend('Value Function')

xlabel('Asset')

ylabel('Value')

subplot(1,2,2)

plot(a_grid,C)

legend('Policy Function')

xlabel('Asset')

ylabel('Consumption')

Sometimes, people use “max” to find value function.

Let’s re-run clear code cell, and parameters code cell.

clear all; % Clears all variables from the workspace

close all; % Closes all open figure windows

clc; % Clears the Command Window

%% Preparation

% Households

y = 1; % Fixed income received by the agent

gamma = 1; % risk aversion in consumption utility function

r = 0.03; % The rate at which savings grow

beta = 0.95; % How much future utility is worth today

% Assets grids

a_grid_size = 500; % Number of asset grid

a_max = 20; % Maximum value of asset

borrow_limit = 0; % Borrowing limit

a_grid_power = 1; % Power of grid interval, 1 for linear, 0 for L-shaped

a_grid = linspace(0,1,a_grid_size)';

a_grid = a_grid.^(1./a_grid_power);

a_grid = borrow_limit + (a_max - borrow_limit).*a_grid;

% Iteration setting

iter_max = 100; % maxium iteration

iter_counter = 1; % iteration counting

iter_tolerance = 0.01; % Tolerance for convergence

iter_diff = 1; % initial difference

%% Initialize value functions and consumption function

V_guess = u(r.*a_grid+y)./(1-beta); % initial guess of value function

V_current = zeros(a_grid_size,1); % current value functions from iteration

V_next = zeros(a_grid_size,1); % new value functions from iteration

V_intermediate = zeros(a_grid_size, iter_max); % intermediate value functions

C = zeros(a_grid_size,1); % consumption policy

S = zeros(a_grid_size,1); % saving function

S_index = zeros(a_grid_size,1); % saving choice index function

%% Local Function to Facilitate Expression

% Utility function

if gamma == 1

u = @(c)log(c);

else

u = @(c)(c.^(1-gamma)-1)./(1-gamma);

end

% Derivative of utility function to consumption

u1 = @(c) c.^(-gamma);

We use “max” here to find optimal choice.

%% Iteration using max

V_next = V_guess;

tic;

while iter_counter <= iter_max && iter_diff > iter_tolerance

iter_counter = iter_counter + 1;

V_current = V_next; % pass the old value to current value

% loop over assets

for i = 1:a_grid_size

cash = (1+r).*a_grid(i) + y;

V_choice = u(max(cash-a_grid,1.0e-10)) + beta.*V_current;

[V_next(i),S_index(i)] = max(V_choice);

S(i) = a_grid(S_index(i)); % Saving = i_th a_grid which maximize value function

C(i) = cash - S(i); % Consumption = cash - saving

end

iter_diff = max(max(abs(V_next - V_current)));

% disp(['Iteration no. ' int2str(iter_counter), ' max val fn diff is ' num2str(iter_diff)]);

end

% Displays the total number of iterations and the time taken

fprintf('Total iteration: %3i, Time: %2.6f \n', iter_counter, toc);

Total iteration: 32, Time: 0.266263

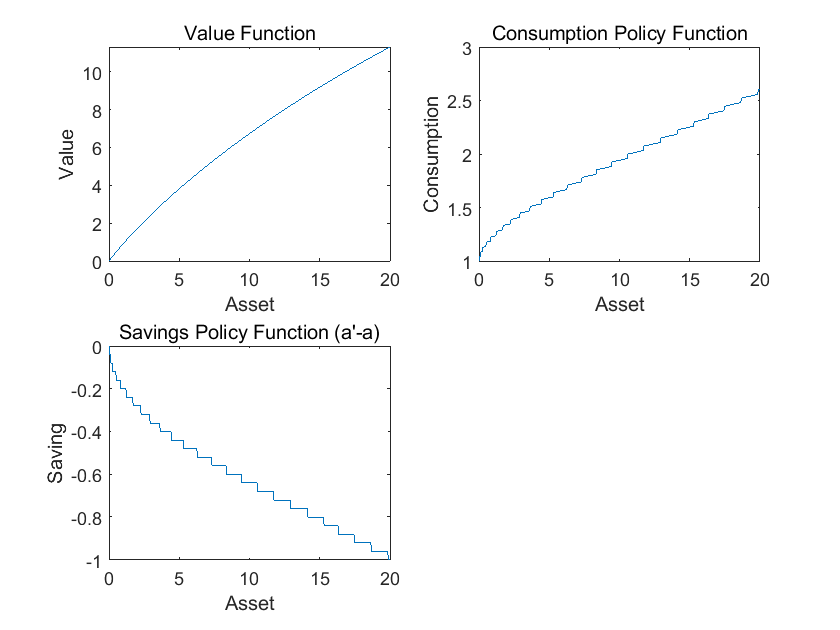

%% Plotting

figure(1)

subplot(2,2,1)

plot(a_grid,V_current)

title('Value Function')

xlabel('Asset')

ylabel('Value')

subplot(2,2,2)

plot(a_grid,C)

title('Consumption Policy Function')

xlabel('Asset')

ylabel('Consumption')

subplot(2,2,3)

plot(a_grid,S-a_grid)

title('Savings Policy Function (a''-a)')

xlabel('Asset')

ylabel('Saving')

This method is much more faster. But there is no interpolation, only find certain index. So, there is zig-zag thing in policy function.

3. Optimal Consumption with Income Shock#

Now we introduce new changes to the problem.

The agent faces three possible income levels: $\( Y = [0.5, 1.0, 1.5] \)$

Each income level has an equal probability: $\( Pi_Y = [\frac{1}{3}, \frac{1}{3}, \frac{1}{3}] \)$

For each combination of asset levels and income states, we need to uses the

fminconoptimization function to determine the optimal consumption level C that maximizes the expected utility:\[ \max_{c} \left\{ -\log(c) - \beta \sum_{j=1}^{3} \Pi_Y(j) V_0(A', Y(j)) \right\} \]The future assets A’ after consumption are calculated based on the current assets, income, and chosen consumption.

In parameter section, here are newly added code lines:

Y = [0.5;1.0;1.5]; % Income levels

Pi_Y = [1/3; 1/3; 1/3]; % Income probabilitie

N_Y = length(Y); % Number of income levels

Others are the same, except for more abbreviation.

%% Preparation

% Households

Y = [0.5;1.0;1.5]; % Income levels

Pi_Y = [1/3; 1/3; 1/3]; % Income probabilities

r = 0.02; % The rate at which savings grow

beta = 0.96; % How much future utility is worth today

% Asset grid

A = (0:0.05:10)'; % Grid of asset from 0 to 10, increments of 0.05

N_A = length(A); % Number of points in the asset grid

N_Y = length(Y); % Number of income levels

% Maximum iterations

Max_iter = 100; % maxium iteration

iter = 1; % iteration start from 1

% Tolerance for convergence

tol = 0.01; % tolerance, larger to shorten time

max_diff = 1; % difference start

% Options for fmincon optimization

opts = optimoptions('fmincon','Display','off','TolX',1.0e-6);

% Initialize value function and consumption

V_0 = zeros(N_A, N_Y); % current value functions

V_1 = zeros(N_A, N_Y); % next value functions

C = zeros(N_A, N_Y); % consumption policy

V_save = zeros(N_A, N_Y, Max_iter); % intermediate value functions

In iteration section, the changes are:

Introduce another loop because of 3 income level.

Future value in Bellman function now is expected value weighted by income probability.

%% Iteration

tic

while max_diff > tol

for j = 1:N_Y

for i = 1:N_A

% Optimize consumption and update value function

utility_function = @(x) -log(x) ...

- beta * (Pi_Y(1)*interp1(A, V_0(:,1), (1+r)*(A(i) + Y(j) - x)) ...

+ Pi_Y(2)*interp1(A, V_0(:,2), (1+r)*(A(i) + Y(j) - x)) ...

+ Pi_Y(3)*interp1(A, V_0(:,3), (1+r)*(A(i) + Y(j) - x)));

[C(i,j), V_1(i,j)] = fmincon(utility_function, ...

0.5*Y(j)+0.5*A(i),[],[],[],[],eps,A(i)+Y(j),[],opts);

end

end

% Update the value function and check for convergence

V_1 = -V_1;

V_save(:,:,iter) = V_1;

max_diff = max(max(abs(V_0 - V_1)));

if mod(iter, 10) == 1

fprintf('Iteration: %d, Max difference: %.8f\n', iter, max_diff);

end

V_0 = V_1;

iter = iter + 1;

end

fprintf('Total iteration: %3i, Time: %2.6f \n', iter, toc);

Iteration: 1, Max difference: 2.44234702

Iteration: 11, Max difference: 0.10095394

Iteration: 21, Max difference: 0.01114086

Total iteration: 25, Time: 46.076386

The plotting section is the same.

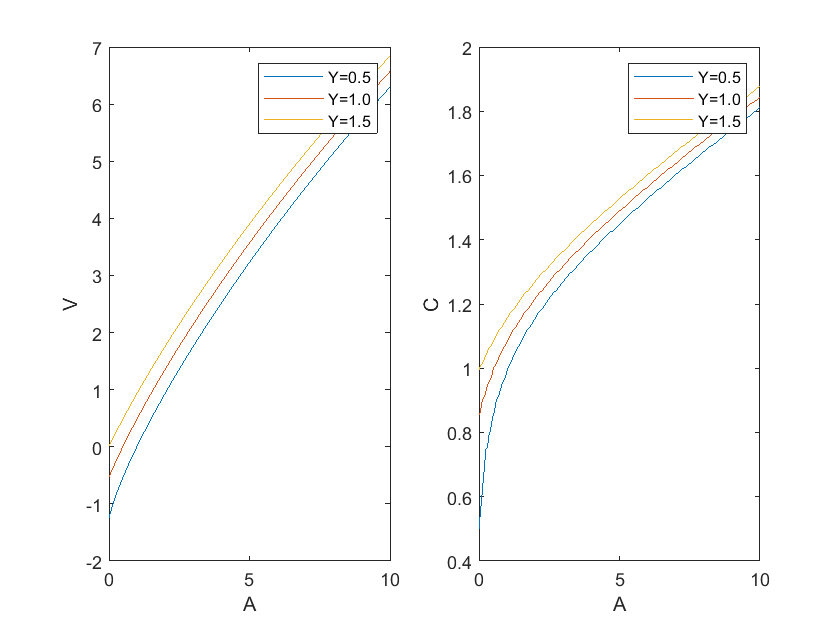

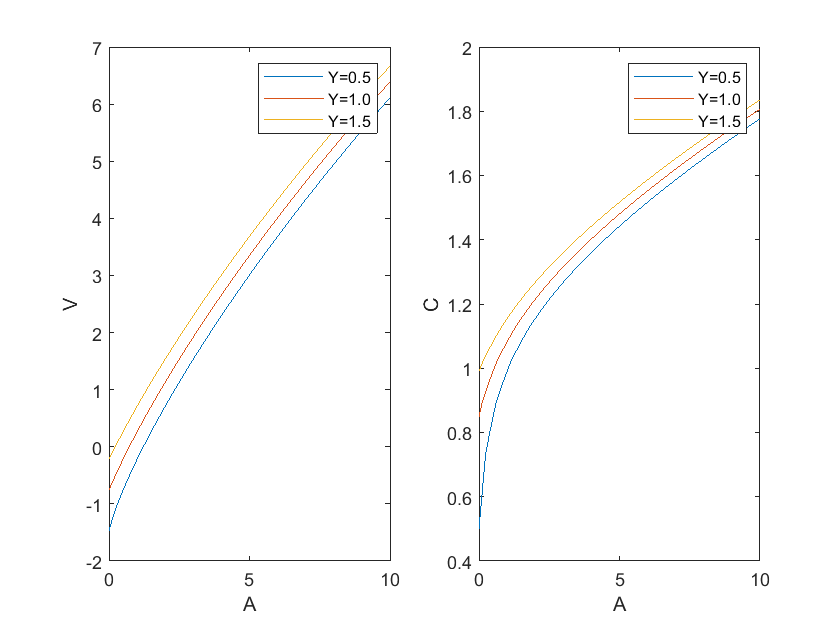

%% Plotting the value function for each income level

figure(1)

subplot(1,2,1)

plot(A, V_1(:,1), A, V_1(:,2), A, V_1(:,3))

legend('Y=0.5','Y=1.0','Y=1.5')

xlabel('A')

ylabel('V')

% Plotting the optimal consumption level for each income level

subplot(1,2,2)

plot(A, C(:,1), A, C(:,2), A, C(:,3))

legend('Y=0.5','Y=1.0','Y=1.5')

xlabel('A')

ylabel('C')

Now, there are many asset grid and several income levels, so we have a nested loop inside a loop.

The computation takes much longer time than the case with constant income.

4. Optimal Consumption Solution 2: Speed Up with Vectorization#

Now we solve the model with value function iteration which is vertorized.

In preparation section, the key difference is how to initialize grids.

%% Preparation

% Households

ygrid = [0.5; 1.0; 1.5]; % Income levels

pi_y = repmat([1/3, 1/3, 1/3], 3, 1); % Income probabilities

r = 0.02; % The rate at which savings grow

beta = 0.96; % How much future utility is worth today

% Asset grid

agrid = (0:0.05:10)'; % Grid of asset from 0 to 10, increments of 0.05

NA_grid = length(agrid); % Number of points in the asset grid

NY_grid = length(ygrid); % Number of income levels

% Maximum iterations

maxiter = 10^(3); % maxium iteration

iter = 1; % iteration start from 1

% Tolerance for convergence

tol_in = 1e-4; % tolerance

max_diff = tol_in + 1; % difference start

% Initialize grids

V_0 = zeros(NA_grid, NY_grid); % current value functions

[AIND,YIND] = ndgrid(1:NA_grid,1:NY_grid);

Amat = agrid(AIND);

Ymat = ygrid(YIND);

% ndgrid creates matrices AIND and YIND for indexing purposes,

% helping to construct matrices of asset and income levels.

% Remember that in previous version, we use following code

% to initialize value function and consumption

% V_0 = zeros(N_A, N_Y); % current value functions

% V_1 = zeros(N_A, N_Y); % next value functions

% C = zeros(N_A, N_Y); % consumption policy

In iteration, we use Golden section method and a function written by Professor Jinhui Bai.

Note that in previous version, we use two loops to check each income level (N_Y) and each asset grids (N_A), one by one.

Here we use vectors, Amat(:)+Ymat(:), to avoid loops. In a single N_Y*N_A matrix, all income level and all asset grids are checked.

Which means, we can check N_Y*N_A element everytime.

So, the computation is much faster.

%% Iteration

disp('vfi loop, running...');

tic

while (max_diff > tol_in && iter < maxiter)

% Objective function for goldenx

objFun = @(x) log(x) + beta * sum(pi_y(YIND(:), :) .* ...

interp1(agrid, V_0, (1+r)*(Amat(:)+Ymat(:)-x),'spline'), 2);

% Optimization

[C, V_1] = GoldenVec(objFun, eps * ones(NA_grid * NY_grid, 1), ...

Amat(:) + Ymat(:), 1000, 1e-8);

V_1 = reshape(V_1, NA_grid, NY_grid);

max_diff = max(abs(V_0(:) - V_1(:)));

V_0 = V_1;

% Display progress every 50 iterations

if mod(iter, 50) == 1

fprintf('Iteration: %d, Max difference: %.8f\n', iter, max_diff);

end

iter = iter + 1;

end

fprintf('vertorized vfi total iteration: %3i, time: %2.6f \n',iter,toc);

%% GoldenVec function by Professor Jinhui Bai

function [x1, f1, exitflag] = GoldenVec(f, a, b, maxiter, tol, varargin)

% GOLDENX computes the local maximum of a univariate function on an interval using Golden Search.

% This function is a vectorized version of the Golden Search method.

%

% Inputs:

% f : name of the function to be maximized. The function should be in the form fval=f(x).

% a, b : left and right endpoints of the interval.

% maxiter : maximum number of iterations.

% tol : convergence tolerance.

% varargin: optional additional arguments for the function f.

%

% Outputs:

% x1 : local maximum of the function f.

% f1 : function value at the local maximum.

% exitflag: condition of exit (1 = converged, 0 = maximum iteration reached).

% Copyright (c) 1997-2002, Paul L. Fackler & Mario J. Miranda

% paul_fackler@ncsu.edu, miranda.4@osu.edu

% Revised by Jinhui Bai, January 15, 2005

% Check if bracketing points have correct sizes and values

if ~isequal(size(a), size(b))

error('Bracketing vectors must be of the same length.');

end

if any((b - a) <= 0)

error('Lower and upper interval points are not in the correct sequence.');

end

% Define the Golden Section coefficients

alpha1 = (3 - sqrt(5)) / 2;

alpha2 = 1 - alpha1;

% Initialize section points and function evaluations

d = b - a; % Length of the interval

x1 = a + alpha1 * d; % Left section point

x2 = a + alpha2 * d; % Right section point

s = ones(size(x1));

f1 = feval(f, x1, varargin{:});

f2 = feval(f, x2, varargin{:});

% Iteration until convergence or maximum iteration is reached

iter = 0;

while any(d > tol) && (iter <= maxiter)

d = d * alpha2;

i = f2 > f1;

x1(i) = x2(i);

f1(i) = f2(i);

d12 = (alpha2 - alpha1) * d; % Distance between two section points

x2 = x1 + s .* (i - (~i)) .* d12;

s = sign(x2 - x1);

f2 = feval(f, x2, varargin{:});

iter = iter + 1;

end

% Return the larger of the two

i = f2 > f1;

x1(i) = x2(i);

f1(i) = f2(i);

% Define the exit flag

if all(d <= tol)

exitflag = 1;

else

exitflag = 0;

end

end

vfi loop, running...

Iteration: 1, Max difference: 2.44234704

Iteration: 51, Max difference: 0.00319405

Iteration: 101, Max difference: 0.00041483

vertorized vfi total iteration: 137, time: 0.366026

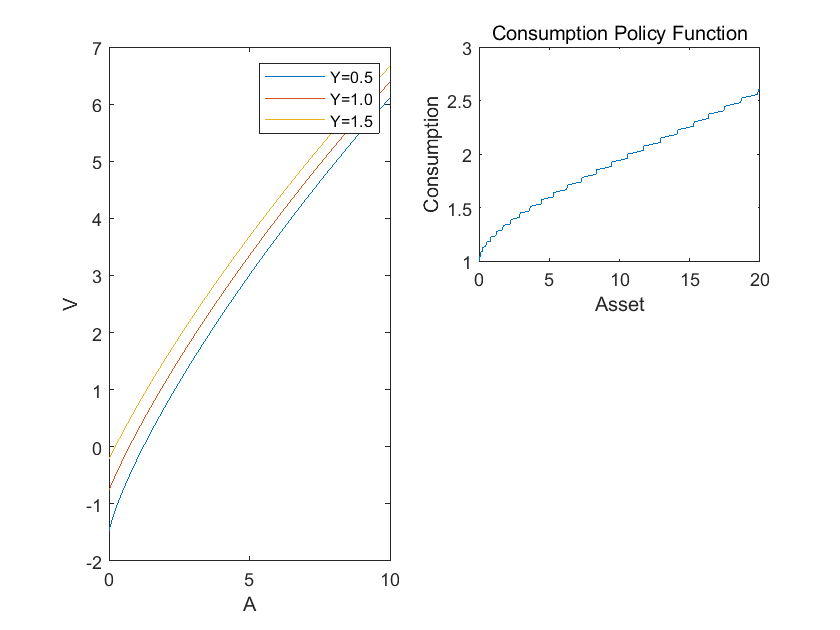

%% Plotting

C = reshape(C, NA_grid, NY_grid);

figure(1);

subplot(1,2,1);

plot(agrid, V_1(:,1), agrid, V_1(:,2), agrid, V_1(:,3));

xlabel('A');

ylabel('V');

legend(arrayfun(@(y) sprintf('Y=%.1f', y), ygrid,'UniformOutput',false));

subplot(1,2,2);

plot(agrid, C);

xlabel('A');

ylabel('C');

legend(arrayfun(@(y) sprintf('Y=%.1f', y), ygrid,'UniformOutput',false));

5. Endogenous Grid Method#

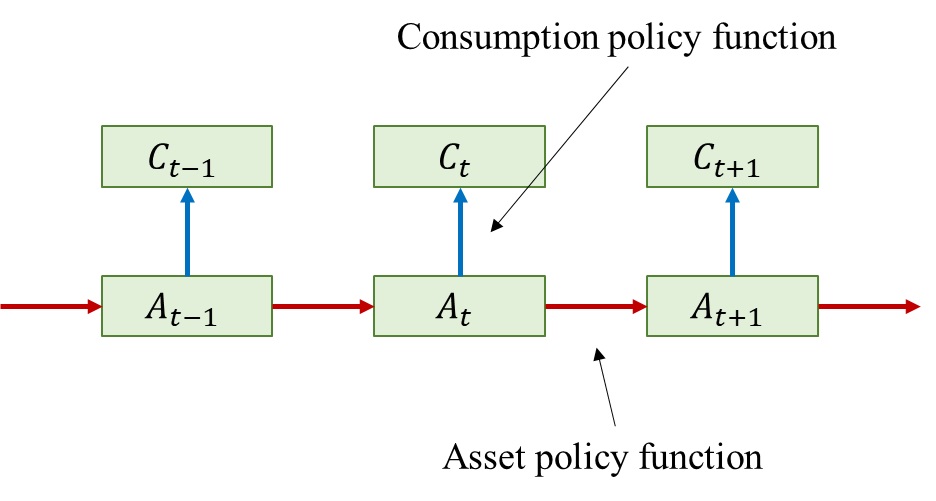

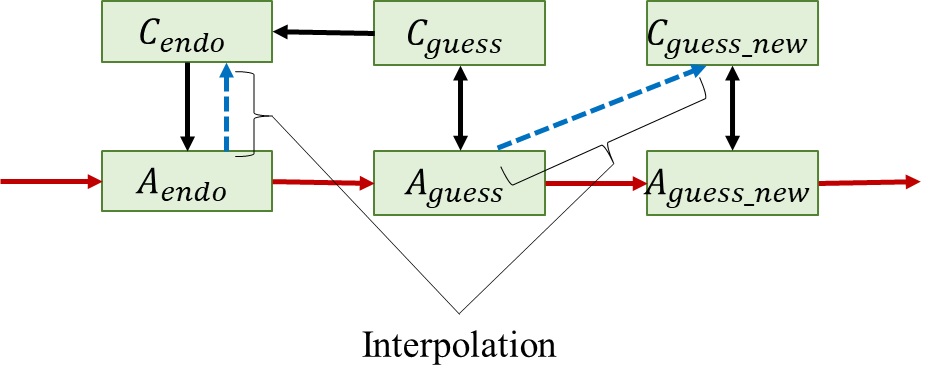

We need to find the consumption policy function (blue arrow) and asset policy function (red arrow).

That is, given \(A_t\), we need to know \(C_t\) and \(A_{t+1}\).

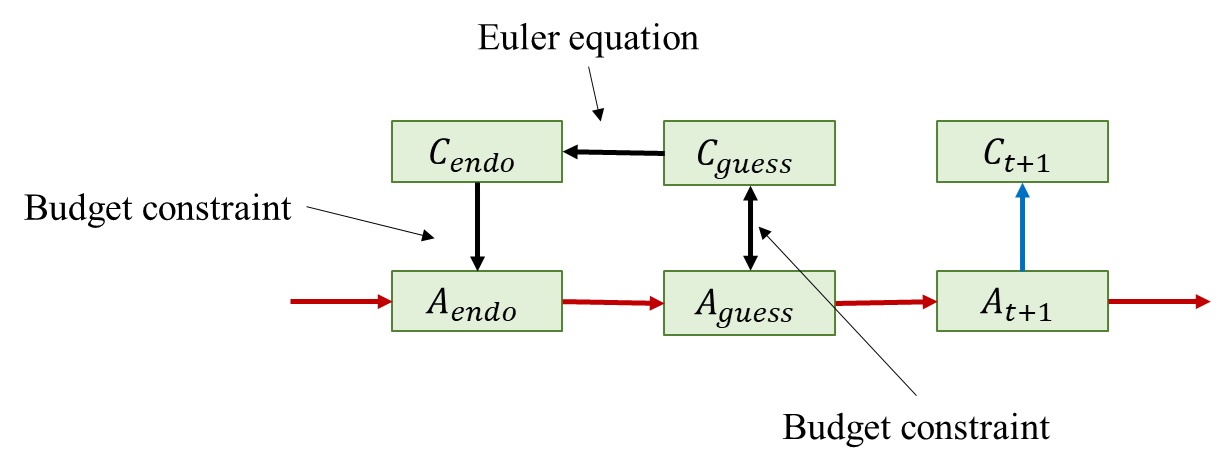

We have a guess value for \(C_t\). Or a guess value for \(A_t\), they are connected by budget constraint.

With Euler equation, we solve for an endogenou \(C_{endo}\). And with budget constraint, we ge \(C_{endo}\).

The calculation is in the black arrows.

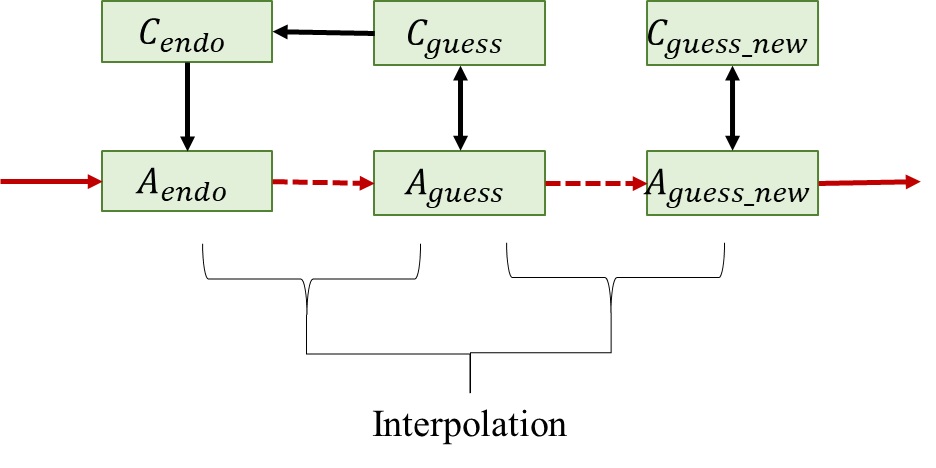

Now we have relation between \(A_{endo}\) and \(A_{guess}\).

We can get a new guess value \(A_{guessnew}\) with this relation using interpolation, and a new guess value \(A_{guessnew}\) by budget constraint.

Then iterate, until two guess values are close enough.

Sometimes, people interpolate the consumption function.

Using the relation betwee \(C_{endo}\) an \(A_{endo}\), we can get a new guess valu \(C_{guessnew}\) starting fro \(A_{guess}\), and then ge \(A_{guessnew}\) by budget constraint.

Then iterate, until new guess values are close enough.

You may ask why we use backward induction, why not forward induction like in the graph.

The main reason is that,\(C_{endo}\) can be written explicitly in backward induction, which is computationally fast.

If we use forward induction, we still need to solve a nonlinear function.

6. Optimal Consumption Solution 3: Speed Up with Endogenous Grid Method#

In preparation section, it’s the same.

%% Preparation

% Households

ygrid = [0.5; 1.0; 1.5]; % Income levels

pi_y = repmat([1/3, 1/3, 1/3], 3, 1); % Income probabilities

r = 0.02; % The rate at which savings grow

beta = 0.96; % How much future utility is worth today

% Asset grid

agrid = (0:0.05:10)'; % Grid of asset from 0 to 10, increments of 0.05

NA_grid = length(agrid); % Number of points in the asset grid

NY_grid = length(ygrid); % Number of income levels

% Maximum iterations

maxiter = 10^(3); % maxium iteration

iter = 1; % iteration start from 1

% Tolerance for convergence

tol_in = 1e-4; % tolerance

max_diff = tol_in + 1; % difference start

% Initialize grids

V_0 = zeros(NA_grid, NY_grid); % current value functions

[AIND,YIND] = ndgrid(1:NA_grid,1:NY_grid);

Amat = agrid(AIND);

Ymat = ygrid(YIND);

% ndgrid creates matrices AIND and YIND for indexing purposes,

% helping to construct matrices of asset and income levels.

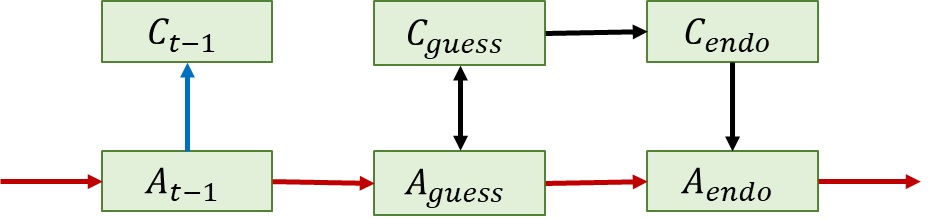

Here in iteration, we don’t have to deal with optimization problem, just pure iteration.

We have:

interp1(a0(:,i),c0(:,i),Amat(:,i),'spline')

a0 and c0 is endogenous changed, this is why it’s called endogenous grid method.

Remember that in Value function iteration, the code is:

interp1(agrid, V_0, (1+r)*(Amat(:)+Ymat(:)-x)

The grids are exogenous there.

Also, in EGM (endogenous grid method), interpolation is used to get optimal policy function,

while, in VFI (value function iteration), interpolation is used to fit data to existing exogenous grid, optimal value function is achieved by fmincon or other opizationmal function.

%% Iteration

% Initial guess on future consumption.

cp0 = r*Amat+Ymat; % cp is consumption projected

cpnext = cp0;

disp('endogenous grid loop, running...');

tic

while (max_diff > tol_in && iter < maxiter)

% Derive current consumption and current assets

% Given guessed future consumption, we can get current consumption

% and current asset, thus their mapping relation,

% or consumption policy function.

c0 = (beta*(1+r)*(cp0.^(-1))*pi_y').^(-1); % from Euler equation

a0 = Amat/(1+r)+c0-Ymat; % from budget constraint

V = log(c0);

% Update the guess for the consumption decision

% Interpolation conditional on productivity realization

% use default option for outbounders (no extrapolation)

for i = 1:3

cpnext(:,i) = interp1(a0(:,i),c0(:,i),Amat(:,i),'spline');

end

% Consumption decision rule for a binding borrowing constraint

idcon = (Amat+Ymat-cpnext)<0;

cpnext(idcon) = Amat(idcon)+Ymat(idcon);

% Compute and display distance

max_diff = max(abs(cpnext(:)-cp0(:)));

if mod(iter,50) == 1

fprintf('Iteration: %d, Max difference: %.8f\n', iter, max_diff);

end

% Update iteration parameters

iter = iter+1;

cp0 = cpnext;

c0 = cpnext;

end

fprintf('endogenous grid total iteration: %3i, time: %2.6f \n',iter,toc);

endogenous grid loop, running...

Iteration: 1, Max difference: 0.64808303

Iteration: 51, Max difference: 0.00021198

endogenous grid total iteration: 56, time: 0.019076

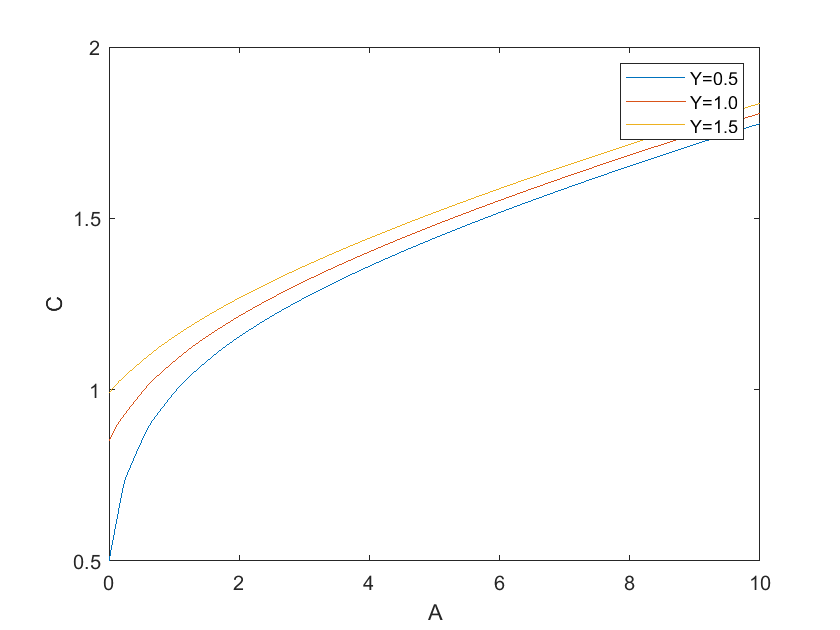

%% Plot results

figure(2);

plot(agrid, cp0);

xlabel('A');

ylabel('C');

legend(arrayfun(@(y) sprintf('Y=%.1f', y), ygrid,'UniformOutput',false));

Reference#

Benjamin Moll, “Solving the Income Fluctuation Problem: Numerical Dynamic Programming”, https://benjaminmoll.com/wp-content/uploads/2021/04/Lecture2_EC442_Moll.pdf

Benjamin Moll, “Heterogeneous-Agent Models and Methods”, https://benjaminmoll.com/wp-content/uploads/2021/04/STEG_course.pdf