1.6 RBC Model in Python#

The algorithm is the same as that we ues in MATLAB case.

Import Module#

# !pip install autograd # if you use autograd for the first time

import autograd.numpy as np

import math

from autograd import jacobian

np.set_printoptions(suppress=True,precision=4)

import autograd.numpy as np: This imports the numpy library but uses Autograd’s version, which allows for automatic differentiation. This is useful for optimization and sensitivity analysis.

np.set_printoptions(suppress=True, precision=4): This sets the printing options for NumPy arrays, suppressing scientific notation and limiting the precision of printed numbers to 4 decimal places.

Indexing#

nX = 8

nEps = 1

iA, iR, iN, iK, iY, iC, iI, iW = range(nX)

nX = 8: This defines the number of state variables in the model (5 in this case).

nEps = 1: This defines the number of shocks (1 in this case).

iA, iR, iN, iK, iY, iC, iI, iW = range(nX): This creates indices for the state variables:

iA (technology level), iR (interest rate), iN (working hour), iK (capital), iY (output), iC (consumption), iI (investment), iW (wage).

Parameters#

alpha = 0.35 # capital share

beta = 0.99 # discount factor

gamma = 1 # risk aversion

eta = 1 # labor elasticity

delta = 0.025 # depreciation rate

rho = 0.95 # TFP persistency

phi = 7.8 # labor disutility

Model parameters are defined:

alpha: Output elasticity of capital.

beta: Discount factor for future utility.

gamma: Coefficient of relative risk aversion.

delta: Depreciation rate of capital.

rho: Persistence of technology shocks.

def SteadyState():

A = 1

R = 1 / beta - 1 + delta

N = 1/3

K = N * (R/A/alpha)**(1/(alpha-1))

Y = A * K**alpha * N**(1-alpha)

C = Y - delta * K

I = delta*K

W = (1-alpha)*Y/N

X = np.zeros(nX)

X[[iA, iR, iN, iK, iY, iC, iI, iW]] = (A, R, N, K, Y, C, I, W)

return X

def SteadyState(): This defines a function to calculate the steady state of the model.

A = 1.: Sets the technology level (Z) to 1.

R = 1 / beta - 1 + delta: Calculates the steady-state interest rate.

K = N * (R/A/alpha)^(1/(alpha-1)): Calculates the steady-state capital stock using the given parameters.

Y = A * K^alpha * N^(1-alpha): Calculates output (Y) using the Cobb-Douglas production function.

C = Y - delta * K: Calculates consumption (C) as the output minus depreciation on capital.

X = np.zeros(nX): Initializes a vector X of zeros to store state variables.

X[[iA, iR, iN, iK, iY, iC, iI, iW]] = (A, R, N, K, Y, C, I, W): Assigns the calculated values to the corresponding indices in X.

X_SS = SteadyState()

epsilon_SS = 0.0

print("Steady state: {}".format(X_SS))

Steady state: [ 1. 0.0351 0.3333 11.4661 1.1499 0.8633 0.2867 2.2423]

X_SS = SteadyState(): Calls the SteadyState function and stores the result in X_SS.

epsilon_SS = 0.0: Initializes the steady-state value of the shock to zero.

Model equations#

def F(X_Lag, X, X_Prime, epsilon):

# Unpack. The state variables are unpacked from the input vectors X_Lag, X, and X_Prime.

A, R, N, K, Y, C, I, W = X

A_L, R_L, N_L, K_L, Y_L, C_L, I_L, W_L = X_Lag

A_P, R_P, N_P, K_P, Y_P, C_P, I_P, W_P = X_Prime

return np.hstack((

beta * (1+R-delta) * C_P**(-1/gamma) * C**(1/gamma) - 1.0, # Euler equation

phi * N**(1/eta) - W*C**(-1/gamma),

A * K_L**alpha * N**(1-alpha) - Y, # Production function

alpha * A * K_L**(alpha-1) * N**(1-alpha) - R, # MPK

(1-alpha) * A * K_L**alpha * N**(-alpha) - W, # MPN

(1 - delta) * K_L + I_L - K, # Aggregate resource constraint

# Do not use (1 - delta) * K + I - K_P

Y - C - I, # Aggregate resource constraint

rho * np.log(A_L) + epsilon - np.log(A) # TFP evolution

))

To calculate power result, we use ^ in MATLAB, and use ** in Python.

And to calculate log, we directly use log in MATLAB, and use np.log in Python.

def F(X_Lag, X, X_Prime, epsilon): Defines a function F that contains the model equations.

Returns a stacked array with the 8 equations we discussed above.

numpy.hstack() function is used to stack the sequence of input arrays horizontally (i.e. column wise) to make a single array.

Check steady state#

When we select a proper \(\phi\), we should get an array consists of zeros, or close to zero.

F(X_SS,X_SS,X_SS,epsilon_SS)

array([0. , 0.0025, 0. , 0. , 0. , 0. , 0. , 0. ])

Linearize#

A = jacobian(lambda x: F(X_SS,X_SS,x,epsilon_SS))(X_SS)

B = jacobian(lambda x: F(X_SS,x,X_SS,epsilon_SS))(X_SS)

C = jacobian(lambda x: F(x,X_SS,X_SS,epsilon_SS))(X_SS)

E = jacobian(lambda x: F(X_SS,X_SS,X_SS,x))(epsilon_SS)

print("A: {}".format(A))

print("B: {}".format(B))

print("C: {}".format(C))

print("E: {}".format(E))

A: [[ 0. 0. 0. 0. 0. -1.1584 0. 0. ]

[ 0. 0. 0. 0. 0. 0. 0. 0. ]

[ 0. 0. 0. 0. 0. 0. 0. 0. ]

[ 0. 0. 0. 0. 0. 0. 0. 0. ]

[ 0. 0. 0. 0. 0. 0. 0. 0. ]

[ 0. 0. 0. 0. 0. 0. 0. 0. ]

[ 0. 0. 0. 0. 0. 0. 0. 0. ]

[ 0. 0. 0. 0. 0. 0. 0. 0. ]]

B: [[ 0. 0.99 0. 0. 0. 1.1584 0. 0. ]

[ 0. 0. 7.8 0. 0. 3.0089 0. -1.1584]

[ 1.1499 0. 2.2423 0. -1. 0. 0. 0. ]

[ 0.0351 -1. 0.0684 0. 0. 0. 0. 0. ]

[ 2.2423 0. -2.3545 0. 0. 0. 0. -1. ]

[ 0. 0. 0. -1. 0. 0. 0. 0. ]

[ 0. 0. 0. 0. 1. -1. -1. 0. ]

[-1. 0. 0. 0. 0. 0. 0. 0. ]]

C: [[ 0. 0. 0. 0. 0. 0. 0. 0. ]

[ 0. 0. 0. 0. 0. 0. 0. 0. ]

[ 0. 0. 0. 0.0351 0. 0. 0. 0. ]

[ 0. 0. 0. -0.002 0. 0. 0. 0. ]

[ 0. 0. 0. 0.0684 0. 0. 0. 0. ]

[ 0. 0. 0. 0.975 0. 0. 1. 0. ]

[ 0. 0. 0. 0. 0. 0. 0. 0. ]

[ 0.95 0. 0. 0. 0. 0. 0. 0. ]]

E: [0. 0. 0. 0. 0. 0. 0. 1.]

Calculate the Jacobian matrices for the model equations, which represent how the system responds to small changes in state variables.

The last (X_SS) means evaluating the Jacobian at the point X_SS.

A: How small change of future variables affect the system equilibrium, starting ananlysis from X_SS.

B: How nowadays affect the system.

C: How past affect the system.

E: How exogenous shock affect the system, starting analysis from epsilon_SS.

def SolveSystem(A,B,C,E):

# Solve the system using linear time iteration as in Rendahl (2017)

MAXIT = 1000

P = np.zeros(A.shape)

for it in range(MAXIT):

P = -np.linalg.lstsq(B+A@P,C,rcond=None)[0] # (B+A⋅P)⋅(-P)=C

test = np.max(np.abs(C+B@P+A@P@P)) # C+B*P+A*P*P=0

if test < 1e-7:

break

# Impact matrix

# Solution is x_{t}=P*x_{t-1}+Q*eps_t

Q = -np.linalg.inv(B+A@P) @ E # Q = - E*(B+AP)

return P, Q

P, Q = SolveSystem(A,B,C,E)

print(P)

print(Q)

[[ 0.95 -0. -0. -0. -0. -0. -0. -0. ]

[ 0.0444 -0. -0. -0.0023 -0. -0. -0.0008 -0. ]

[ 0.1614 -0. -0. -0.0052 -0. -0. -0.0121 -0. ]

[ 0. -0. -0. 0.975 -0. -0. 1. -0. ]

[ 1.4543 -0. -0. 0.0235 -0. -0. -0.0271 -0. ]

[ 0.2554 -0. -0. 0.0445 -0. -0. 0.0423 -0. ]

[ 1.1989 -0. -0. -0.0211 -0. -0. -0.0694 -0. ]

[ 1.7502 -0. -0. 0.0807 -0. -0. 0.0285 -0. ]]

[1. 0.0467 0.1699 0. 1.5309 0.2689 1.262 1.8423]

Calls a function SolveSystem to solve the linearized system of equations, returning matrices P and Q.

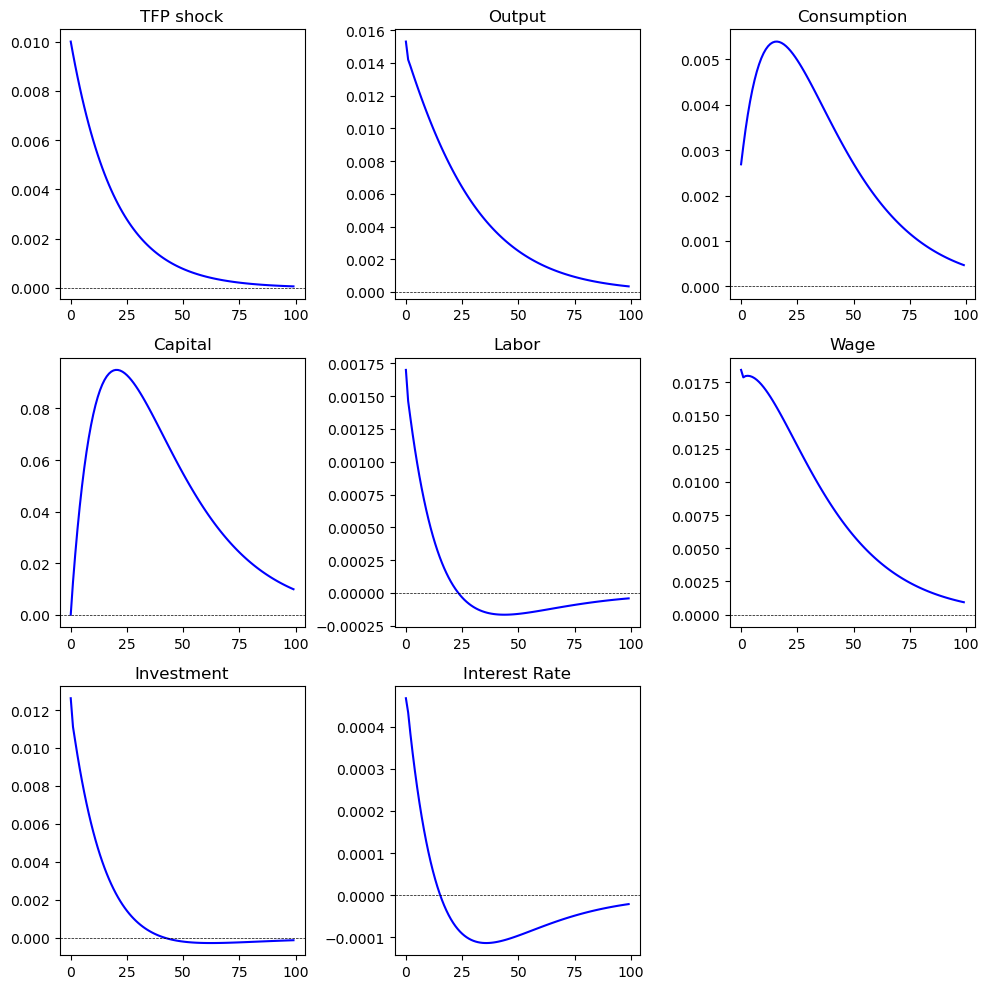

Calculate an impulse response#

IRF_RBC = np.zeros((nX,100))

IRF_RBC[:,0] = Q * 0.01

for t in range(1,100):

IRF_RBC[:,t] = P@IRF_RBC[:,t-1]

IRF_RBC = np.zeros((nX, 100)): Initializes a matrix to store impulse response functions.

IRF_RBC[:, 0] = Q * 0.01: Sets the initial impulse response based on matrix Q.

Loop: Iteratively calculates the impulse responses for 100 periods using the transition matrix P.

In Python, the @ operator is used for matrix multiplication. To convert this line to MATLAB, you will use the * operator instead

Print#

Finally, we plot the impulse response function, which is the same as what we get in MATLAB and Dynare.

import matplotlib.pyplot as plt

import numpy as np

# create a 3x3 subplot

fig, axs = plt.subplots(3, 3, figsize=(10, 10))

# subplot

axs[0, 0].plot(IRF_RBC[iA, :], label='Impulse Response of Output', color='blue')

axs[0, 0].set_title('TFP shock')

axs[0, 0].axhline(0, color='black', lw=0.5, ls='--')

# axs[0, 0].legend()

axs[0, 1].plot(IRF_RBC[iY, :], label='Impulse Response of Output', color='blue')

axs[0, 1].set_title('Output')

axs[0, 1].axhline(0, color='black', lw=0.5, ls='--')

axs[0, 2].plot(IRF_RBC[iC, :], label='Impulse Response of Output', color='blue')

axs[0, 2].set_title('Consumption')

axs[0, 2].axhline(0, color='black', lw=0.5, ls='--')

axs[1, 0].plot(IRF_RBC[iK, :], label='Impulse Response of Output', color='blue')

axs[1, 0].set_title('Capital')

axs[1, 0].axhline(0, color='black', lw=0.5, ls='--')

axs[1, 1].plot(IRF_RBC[iN, :], label='Impulse Response of Output', color='blue')

axs[1, 1].set_title('Labor')

axs[1, 1].axhline(0, color='black', lw=0.5, ls='--')

axs[1, 2].plot(IRF_RBC[iW, :], label='Impulse Response of Output', color='blue')

axs[1, 2].set_title('Wage')

axs[1, 2].axhline(0, color='black', lw=0.5, ls='--')

axs[2, 0].plot(IRF_RBC[iI, :], label='Impulse Response of Output', color='blue')

axs[2, 0].set_title('Investment')

axs[2, 0].axhline(0, color='black', lw=0.5, ls='--')

axs[2, 1].plot(IRF_RBC[iR, :], label='Impulse Response of Output', color='blue')

axs[2, 1].set_title('Interest Rate')

axs[2, 1].axhline(0, color='black', lw=0.5, ls='--')

axs[2, 2].axis('off')

# layout adjustment

plt.tight_layout()

plt.show()